What is driving the fall in gold prices?

Why in the News?

Gold prices have experienced a sharp and unexpected decline since the onset of the West Asian conflict in February 2026, contradicting its historical role as a safe-haven asset. In India, 24-carat gold fell from approximately ₹1.9 lakh per 10 grams in late January to around ₹1.3 lakh per 10 grams, prompting questions about what has changed in the global economic landscape to reverse gold’s typical crisis-time performance.

Background

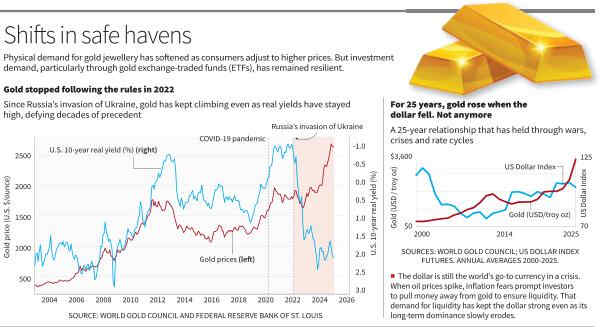

Historically, gold has thrived during crises, surging during the 2008 financial meltdown, the COVID-19 pandemic, and after Russia invaded Ukraine in 2022. Gold’s appeal traditionally stems from two factors:

- Low Interest Rates: As a non-interest-bearing asset, gold becomes more attractive when bond yields fall.

- Weak Dollar: Gold is priced in U.S. dollars globally; a weaker dollar makes it cheaper for foreign buyers, boosting demand.

Before the current conflict, gold had been on a strong run, with international prices exceeding $5,000 per troy ounce and Indian prices more than doubling over two years.

Challenge

- Interest Rate Expectations: The West Asian conflict triggered an oil price surge past $120 per barrel, reigniting inflation fears. Central banks are now expected to keep rates “higher for longer,” making interest-bearing government bonds more attractive than gold.

- Stronger Dollar: Higher expected interest rates have strengthened the dollar as investors flock to dollar-denominated assets. A stronger dollar makes gold more expensive for foreign buyers, dampening demand.

- Liquidity Crunch and Profit Booking: Stock markets have fallen sharply. Investors facing losses in equities have sold profitable gold holdings to cover shortfalls, triggering a cascade of sell orders. Automatic stop-loss mechanisms have exacerbated the downward spiral.

- Dollar’s Haven Status: In the short term, the dollar has reasserted itself as the go-to currency during crises, particularly because oil, now more expensive, must be purchased in dollars, driving up demand for the currency.

Way Forward

- Underlying Demand Remains Strong: Central bank buying, though modestly slower in 2025, rebounded in February 2026. Gold ETF inflows in India remained positive for the tenth consecutive month, and February imports were 80% higher year-on-year despite the price drop.

- Long-Term Fundamentals Intact: The conflict’s trajectory will be key. If oil prices stabilise, rate hike expectations will recede, restoring gold’s appeal. Even in a stagflation scenario (slow growth with high inflation), gold has historically performed well.

- Structural Shift: Following the freezing of Russian assets by Western allies, central banks have pivoted toward gold as a physical asset that cannot be sanctioned-a trend that continues to support long-term demand.

Conclusion

The current gold price correction represents a temporary deviation from historical patterns, driven by shifting interest rate expectations, a strengthening dollar, and short-term liquidity pressures rather than a fundamental loss of gold’s safe-haven status. While short-term volatility is likely to persist as the West Asian conflict evolves, analysts view the correction as a normal market pullback.